| Preserver Ins. Co. v Ryba |

| 2008 NY Slip Op 05305 [10 NY3d 635] |

| June 10, 2008 |

| Kaye, Ch.J. |

| Court of Appeals |

| Published by New York State Law Reporting Bureau pursuant to Judiciary Law § 431. |

| As corrected through Wednesday, August 6, 2008 |

| Preserver Insurance Company, Appellant, v Arthur Ryba et al., Respondents. |

Argued April 29, 2008; decided June 10, 2008

Preserver Ins. Co. v Ryba, 37 AD3d 574, reversed.

Chief Judge Kaye.

At the heart of this dispute between two insurers—in a case where a construction worker allegedly suffered a grave job site injury—is the question whether the employers' liability insurance coverage is limited to $100,000, as specified in the policy, or unlimited. In this case we conclude that it is limited.

On May 17, 2003 Arthur Ryba, a New Jersey construction worker employed by subcontractor East Coast Stucco & Construction, Inc., allegedly fell from scaffolding while performing work on premises in Orangeburg, New York, owned by general contractor Joaquim Almeida. At the time of the incident, East Coast Stucco, a New Jersey company, maintained a workers' compensation and employers' liability policy issued by Preserver Insurance Company, also of New Jersey. This policy was both underwritten and delivered in New Jersey. Despite East Coast's alleged agreement to have Almeida listed in its policy as an additional insured, it failed to do so.

Claiming that Almeida's negligence resulted in his paraplegia, Ryba asserted various causes of action against Almeida including common-law negligence and violations of [*2]Labor Law §§ 200, 240 (1) and § 241 (6). Because Ryba claimed a grave injury, Almeida commenced a third-party action against Ryba's employer, East Coast Stucco, asserting causes of action for common-law indemnification/contribution, contractual indemnification{**10 NY3d at 639} and breach of contract for failure to procure the promised liability insurance.

On April 23, 2004, Preserver commenced this declaratory judgment action and sought summary judgment on the complaint's three causes of action. First, Preserver sought a declaration that it has no duty to defend Almeida's cause of action for contractual indemnification or for breach of contract for failure to procure insurance for Almeida because its policy expressly excludes coverage for any liability assumed under a contract. Second, Preserver argued that it had no duty to defend or indemnify East Coast Stucco against Almeida's cause of action for common-law indemnification because Ryba's accident in Orangeburg, New York, was not necessary or incidental to East Coast Stucco's work in New Jersey. Third, Preserver argued that if it must provide employers' liability insurance, coverage is limited to $100,000 as provided by the policy.

In response, Northern Assurance Company of America (Almeida's homeowners' insurer, incorrectly sued as "One Beacon Insurance Company") cross-moved for summary judgment on all three causes of action, contending that Preserver was time-barred under Insurance Law § 3420 (d) from disclaiming coverage, and that the Preserver policy is limitless as to the amount of coverage.

Supreme Court agreed with Northern, holding that Insurance Law § 3420 (d) applied because Preserver's policy was "issued for delivery" in New York and that Preserver was therefore time-barred from disclaiming coverage. The court then concluded that the policy itself required Preserver to provide unlimited employers' liability coverage.[FN1] The Appellate Division affirmed on both grounds. We now reverse.

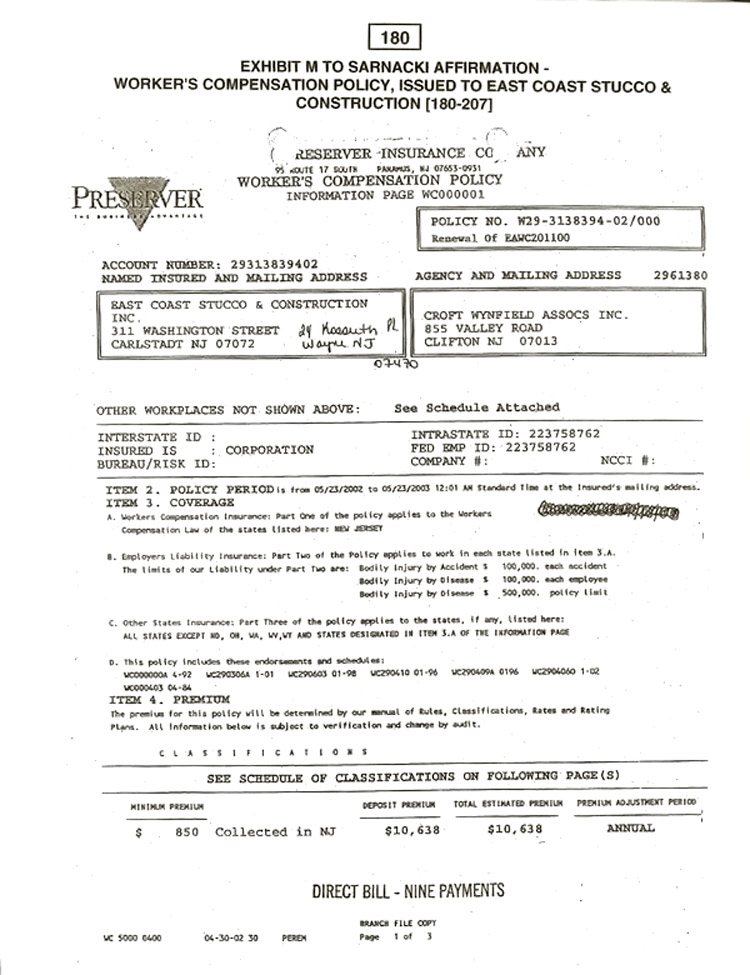

The policy at issue is a standard form workers' compensation and employers' liability contract, mirroring the format and language of model policies that appear in both the New York{**10 NY3d at 640} and New Jersey Workers Compensation and Employers Liability Manuals (the Manuals).[FN2] [*3]

The Information Page. At the front of the policy is an "Information Page," which discloses the policy period ("ITEM 2"), coverage ("ITEM 3") and premium ("ITEM 4"). For ease of reference, a copy of the page is annexed to this writing.

Most notable is "ITEM 3. COVERAGE," which is divided into four subsections (A)-(D), the first three corresponding to various "Parts"—One through Three—found in the body of the policy. In turn, Part One within the policy refers to "Workers Compensation Insurance," Part Two to "Employers Liability Insurance" and Part Three to "Other States Insurance." While the issue here centers on the coverage afforded by Part Two, all three parts provide useful information.

Item 3.A. in the Information Page reads "Workers Compensation Insurance: Part One of the policy applies to the Workers Compensation Law of the states listed here: NEW JERSEY." Item 3.B. states "Employers Liability Insurance: Part Two of the Policy applies to work in each state listed in item 3.A. The limits of our Liability under Part Two are: Bodily Injury by Accident $100,000. each accident."[FN3] Item 3.C. reads: "Other States Insurance: Part Three of the policy applies to the states, if any, listed here: ALL STATES EXCEPT ND, OH, WA, WV, WY AND STATES DESIGNATED IN ITEM 3.A OF THE INFORMATION PAGE."

Part One. Within the body of the policy, "Part One-Workers Compensation Insurance" provides both defense and payment{**10 NY3d at 641} for costs resulting from bodily injuries caused by conditions of the insured's employment. Notably, Part One states: "Terms of this [workers compensation] insurance that conflict with the workers compensation law are changed by this statement to conform to that law."

Part Two. "Part Two-Employers Liability Insurance" contains no similar clause. Indeed, in a subsection titled "Exclusions" the policy makes clear that the employers' liability policy does not cover "any obligation imposed by a workers compensation, occupational disease, unemployment compensation or disability benefits law, or any similar law." Also of note in the "Exclusions" is that the employers' liability policy does not cover "liability assumed under a contract." In a subsection entitled "Limits of Liability," Part Two underscores that

"[o]ur liability to pay for damages is limited. Our limits of liability are shown in Item 3.B. of the Information Page. They apply as explained below.

"1. Bodily Injury by Accident. The limit shown for 'bodily injury by accident-each accident' is the most we will pay for all damages covered by this insurance because of bodily injury to one or more employees in any one accident."

Part Three. Finally, "Part Three-Other States Insurance" states that

"[i]f you begin work in any one of those states [shown in Item 3.C. of the Information Page] after the effective date of this policy and are not insured or are not self-insured for such work, all provisions of the [*4]policy will apply as though that state were listed in Item 3.A. of the Information Page."

Part Three also requires that East Coast "[t]ell us at once if you begin work in any state listed in Item 3.C. of the Information Page" (presumably allowing for increased premiums for increased risk). There is no evidence that East Coast Stucco informed Preserver that it commenced operations on Almeida's New York property.

The policy concludes with several New Jersey endorsements and schedules mirroring stock forms found in the New Jersey Workers Compensation and Employers Liability Insurance Manual. There are no endorsements for New York or any of the other states included in Item 3.C. of the Information Page. Finally, despite East Coast's alleged agreement to have Almeida listed in its policy as an additional insured, he is not.{**10 NY3d at 642}

New York Insurance Law § 3420 (d) provides that when a liability policy is "delivered or issued for delivery in this state, [if] an insurer shall disclaim liability or deny coverage for death or bodily injury . . . it shall give written notice as soon as is reasonably possible." It is undisputed that the policy was actually delivered in New Jersey by a New Jersey insurer to a New Jersey insured. Was the policy nonetheless "issued for delivery" in New York? We answer in the negative.

A policy is "issued for delivery" in New York if it covers both insureds and risks located in this state (see Columbia Cas. Co. v National Emergency Servs., 282 AD2d 346, 347 [1st Dept 2001]; see also American Ref-Fuel Co. of Hempstead v Employers Ins. Co. of Wausau, 265 AD2d 49, 53 [2d Dept 2000]). By including New York as an "Item 3.C." state, the policy covers risks located in New York. East Coast Stucco is, however, a New Jersey company, with its only offices located in that state, so it cannot be said that the insured is located in New York. Because the policy was neither actually "delivered" nor "issued for delivery" in New York, Preserver is not required by Insurance Law § 3420 (d) to make timely disclaimer of coverage.

Further, since the policy explicitly excludes coverage for any liability assumed under a contract, Preserver must neither defend nor indemnify East Coast Stucco for the contractual indemnification or breach of contract causes of action. And even if the policy were "issued for delivery" in New York, Preserver still would not be barred from denying coverage for Almeida's breach of contract claim since Insurance Law § 3420 (d) requires timely disclaimer only for denials of coverage "for death or bodily injury."

By the terms of the policy, under the section entitled "Limits of Liability" in "Part Two-Employers Liability Insurance," Preserver states that its liability for damages is limited as shown in Item 3.B. of the Information Page and that this limit is the most it will pay for bodily injuries to an employee in any one accident. Item 3.B., in turn, states that the "limits of our Liability under Part Two are: Bodily Injury by Accident $100,000. each accident."

Despite this clear limitation on coverage, Northern asks us to construe this contract to require Preserver to provide{**10 NY3d at 643} unlimited employers' liability coverage as if the policy were underwritten in New York, where the New York Manual requires that insurance policies provide unlimited employers' liability coverage. Northern's argument rests first on the fact that New York is included as an Item 3.C. state, and second on the provision of "Part Three—Other States Insurance" that if work begins in a 3.C. state "all provisions of the policy will apply as though that state were listed in Item 3.A. of the Information Page." In short, according to [*5]Northern, being listed as a 3.C. state is the same as being listed as a 3.A. state, and East Coast is entitled to coverage as if the policy were underwritten in New York. This argument misapprehends the plain language of the policy as well as the Manual.

Including New York as "a 3.C. state" means what the policy says it means: that if an accident occurs in such a state, all provisions of the policy will apply. This includes the stated limitation of coverage for employers' liability insurance to $100,000 per accident.

Nothing in the policy suggests that this cap evaporates when an accident occurs in a 3.C. state. Nor, significantly, does Part Two provide—as Part One does—that employers' liability insurance will conform to the workers' compensation laws of the state where the injury occurs. This conclusion is fortified by Part Two's "Exclusions," stating that this portion of the policy does not cover "any obligation imposed by a workers compensation . . . or any similar law." Plainly, nothing in the insurance contract supports Northern's argument for unlimited liability.

Both insurers agree that no statutory provision mandates unlimited employers' liability coverage. Northern, however, asks us to defer to the New York Manual, arguing that it requires insurance policies to provide unlimited employers' liability coverage, a requirement made applicable in this case because the risk took place in New York.

Northern is wrong. Preserver's "Information Page" mirrors sample information pages found in both the New York and New Jersey Manuals. Moreover, both states' manuals contain "Information Page Notes," which explain the terms and requirements of the information page. In both manuals, these Notes state that

"[i]f the [insurance] company learns that the{**10 NY3d at 644} insured is conducting operations in a 3.C. state, and if the company agrees to continue coverage, the company should add that state to Item 3.A. and remove it from Item 3.C. Normal company procedures apply when the state is added to Item 3.A."

Obviously the significance of requiring the insurer to remove a state from 3.C. and add it to 3.A. is that there is a difference between the two categories—they are not automatically coextensive. Moreover, the insurer is required to move a state from 3.C. to 3.A. only if the insured provides notice that it has begun work in a 3.C. state. That did not happen here. In that event, the policy requires the insurer to move the state from 3.C. to 3.A. if it wishes to continue coverage and assume additional risk, presumably including a larger premium.

This last point is confirmed by another portion of the New York Manual, entitled "Rule VIII—Limits of Liability. Item 3.B. of the Information Page." The Manual states that for policies such as Preserver's—which provide both workers' compensation and employers' liability coverage—under Part Two-Employers Liability "[t]here is no limit of liability for employees subject to the New York Workers' Compensation Law. The New York Limit of Liability Endorsement (WC 31 03 08), which must be attached to every policy affording New York coverage, provides for unlimited liability for employees subject to the New York Law." This refers us to the endorsement titled "WC 31 03 08" which, in turn, requires an insurer to state that "We may not limit our liability to pay damages for [employers' liability insurance]." However, this form also explains that "This endorsement applies only . . . because New York is shown in Item 3.A." and a note at the bottom of the document states that this "endorsement must be attached to every policy showing New York in Item 3.A. of the Information Page." [*6]

Plainly, when a state is listed under Item 3.A., the insurer is required to provide a number of additional endorsements that are not required when the state is merely listed in Item 3.C. In East Coast Stucco's policy, which was underwritten in New Jersey, and which lists only New Jersey under Item 3.A., there are several New Jersey endorsements attached to the policy. None, however, provide unlimited employers' liability insurance. Whether New Jersey is listed as a 3.A. or 3.C. state, nothing in the New Jersey Manual requires that an insurer provide unlimited coverage.

The Preserver policy lacks any New York endorsements, precisely because New York is an Item 3.C. state. Here, even if{**10 NY3d at 645} Preserver is bound by the New York Manual, its employers' liability insurance for Ryba's injury should be capped at $100,000 because Preserver was not informed that East Coast was operating in New York. That being so, Preserver was not required to move New York from a 3.C. state to a 3.A. state, and not required to add an endorsement providing unlimited employers' liability insurance for injuries in New York.

Finally, we note that an amendment, effective September 9, 2007, to Workers' Compensation Law § 50 (2), now requires out-of-state employers with operations and/or employees in New York State to maintain workers' compensation insurance "through a policy issued under the law of this state." The New York Workers' Compensation Board has advised that this requirement can only be fulfilled when New York is listed in Item 3.A. of the policy's Information Page (see New York State Insurance Fund, Important Notice to Workers Compensation Insurance Policyholders Who Contract With Out-of-State Subcontractors, available at http://ww3.nysif.com/nysifmedia/pdf/phs/special_notice_to_contractors.pdf [accessed May 9, 2008], cached at http://www.nycourts.gov/reporter/webdocs/special_notice_to_contractors.pdf; see also Workers' Compensation Board, Out-of-State Companies Working in New York State, available at http://www.wcb.state.ny.us/content/main/Carriers/outOfStateReq.jsp [accessed May 9, 2008], cached at http://www.nycourts.gov/reporter/webdocs/out_of_state_companies_working_nys.htm).

Accordingly, the order of the Appellate Division should be reversed, with costs, and judgment granted declaring that plaintiff has no duty to indemnify defendant East Coast Stucco & Construction, Inc. with respect to Almeida's contractual indemnification and breach of contract claims in the underlying action, and that plaintiff's duty to indemnify defendant East Coast Stucco & Construction, Inc. with respect to the remaining claims against it is limited to $100,000.

Judges Ciparick, Graffeo, Read, Smith, Pigott and Jones concur.

Order reversed, etc.

{**10 NY3d at 646}